Key Operational Takeaways.

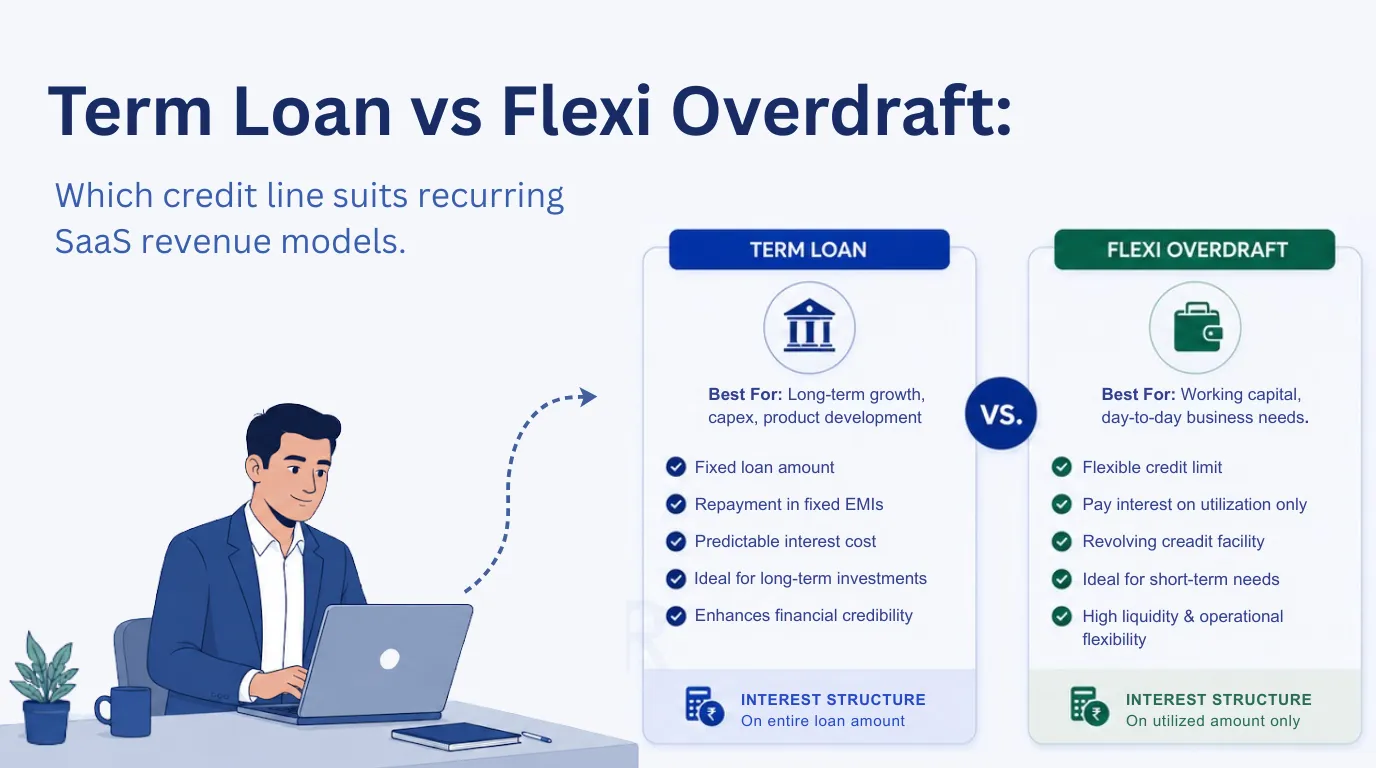

Cash flow cycles in software-as-a-service (SaaS) and subscription-based enterprise models are highly specific. These companies often experience large spikes of capital inflow in certain quarters, as enterprise customers pay their annual renewals of subscriptions, and then a long, slow collection phase, where cash flows are used only to support operations and keep products alive. Massive structural cost inefficiencies are created by forcing a highly cyclical business model into a traditional, rigid Unsecured Term Loan structure.

With a standard term loan you receive the entire principal amount in one lump sum directly into your current account on Day 1. This means that interest begins to accrue immediately on 100% of the capital. If that cash is just sitting in your bank account for 90 days waiting to fund future software or engineering payrolls, you are suffering from serious cash drag.

The optimal capital structure for this situation is an Unsecured Hybrid or Flexi Overdraft (OD) Line. This facility provides a validated credit safety net with interest calculated strictly on the basis of daily reducing balance, which is applied only on the exact rupee value drawn out of the limit.

Real Life Example

A mid-sized SaaS company has bulk contract renewals in April and October, creating huge upfront liquidity. But inflow drops considerably between June and September while the operating costs for cloud engineering talent and data clusters remain perfectly flat.

So, the firm took an Unsecured Term Loan of ₹3 Crore to maintain an operational buffer for these lean months.

The company soon realised that even when there was a lot of cash coming into their existing account from renewal cycles, the bank continued to charge interest on the entire ₹3 Crore principal which was an avoidable interest expense.

The firm restructured its debt architecture by taking this file out of the term loan format and procuring a ₹3 Crore Unsecured Flexi Overdraft facility. Now, during peak renewal months they put their client cash in the account, which brings the drawn limit down to zero and their interest cost down to zero. In dry quarters, they draw down capital on-demand to fund operations, paying interest strictly on the used up balance, saving the company lakhs in annual debt servicing overheads.

Operational Key Learnings

- Eliminate cash drag: Don’t hold fully funded term loans on your balance sheet if the money is going to sit idle waiting for future operational deployment.

- Daily interest accuracy: Flexi Overdraft lines allow you to fine-tune your cash interest costs precisely to your operating requirements, on a daily reducing balance basis.

- Operational Cushion Maintenance – An overdraft line is a live corporate safety net that can be tapped and paid back at any time without prepayment penalty fees.

Enjoying our insights? Never miss an update on Google Discover or Google Reads. ➜