Key operational takeaways.

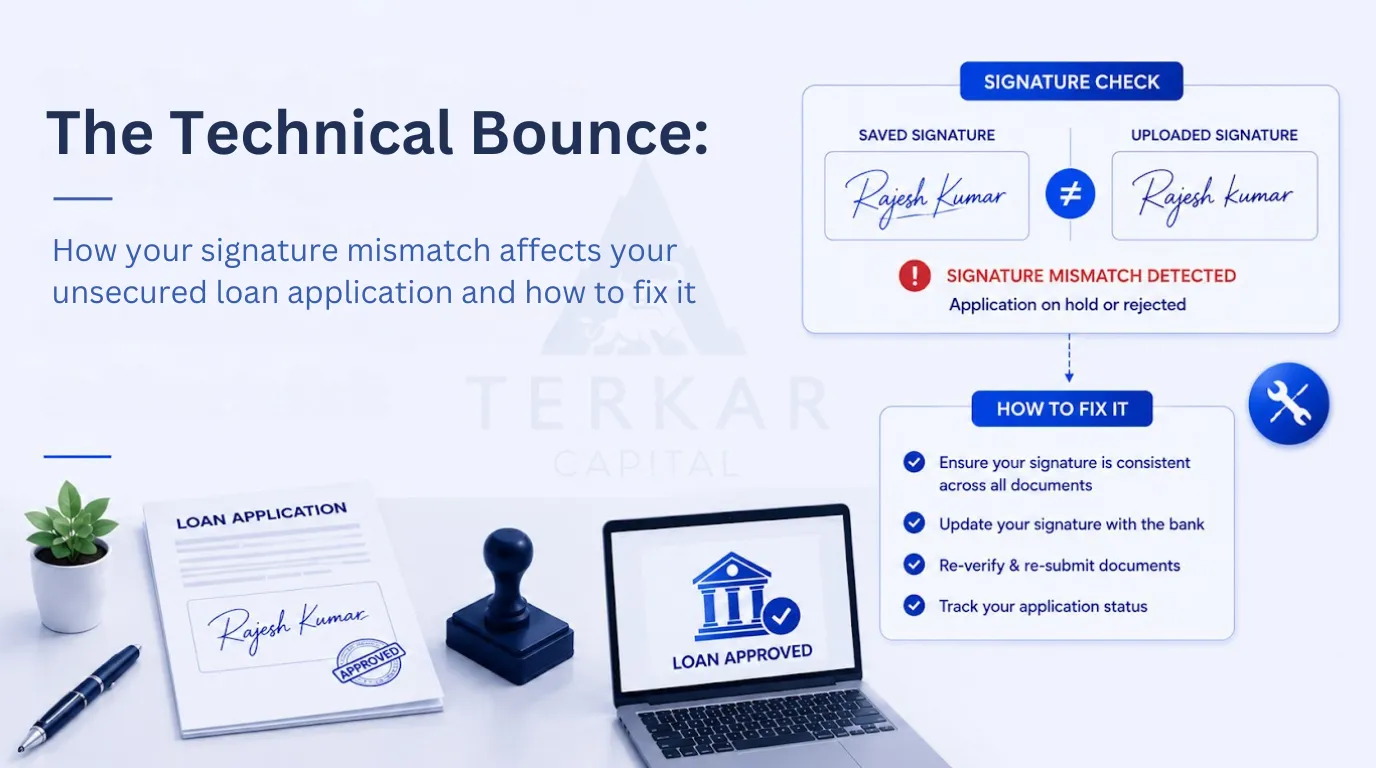

Once you submit a corporate loan application file, your bank statements are automatically processed by automated software systems known as Bank Statement Analyzers. These engines run sophisticated semantic algorithms to filter for financial distress. The most common single trigger for an instant, automated rejection is ongoing transaction bounce flags. The software is designed to treat any outward cheque or auto-debit (NACH) failure as a clear indicator of a severe cash crunch or poor financial discipline.

The system cannot tell the difference between a financial default caused by lack of funds and a completely innocuous administrative mistake like a signature mismatch, an old mandate form or a technical banking routing error.

So now you have to immediately go through a formal Administrative Remediation Protocol to avoid having your file permanently blocked for unsecured credit. This means that you must isolate the error, obtain a clean formal declaration from your bank’s clearing desk and provide hard empirical proof that the underlying payment obligation was settled on the exact same day.

Real World Example:

A corporate enterprise was in the last stages of processing a ₹4 Crore unsecured operational line. The automated analysis tool in the last stage of bank statement extraction identified two different outward cheque bounces in the last month and immediately put the application in a high risk freeze.

The system assumed that the company was stone broke on liquidity.

In fact, the account had a good balance of over ₹50 Lakhs on that particular day and the cheques had bounced only because the promoter had changed his corporate signature profile at a branch office, which resulted in a technical mismatch at the central clearing house .

The firm immediately got a stamped and official Technical Bounce Declaration from their home branch manager which explicitly stated that the error was of administrative nature. An immediate RTGS transaction log was attached which showed the vendor was paid in full hours after the signature alert. The data packet superseded the automated system flag; it showed clean financial intent and the loan would clear final disbursement within forty-eight hours.

Operational Highlights

- Systemic Vulnerability Automated banking-analysis tools are incapable of assessing intent, and so every outward bounce is recorded as an absolute cash-flow default unless otherwise manually adjusted.

- The Bank Declaration Shield: To neutralize systemic credit alerts, an official stamped Technical Bounce Declaration from the clearing desk is needed.

- Same Day Settlement Proof: Always collect immediate alternate payment logs (RTGS or NEFT) to prove you had the underlying liquidity & clean transactional intent.

Enjoying our insights? Never miss an update on Google Discover or Google Reads. ➜