Key Operational Takeaways.

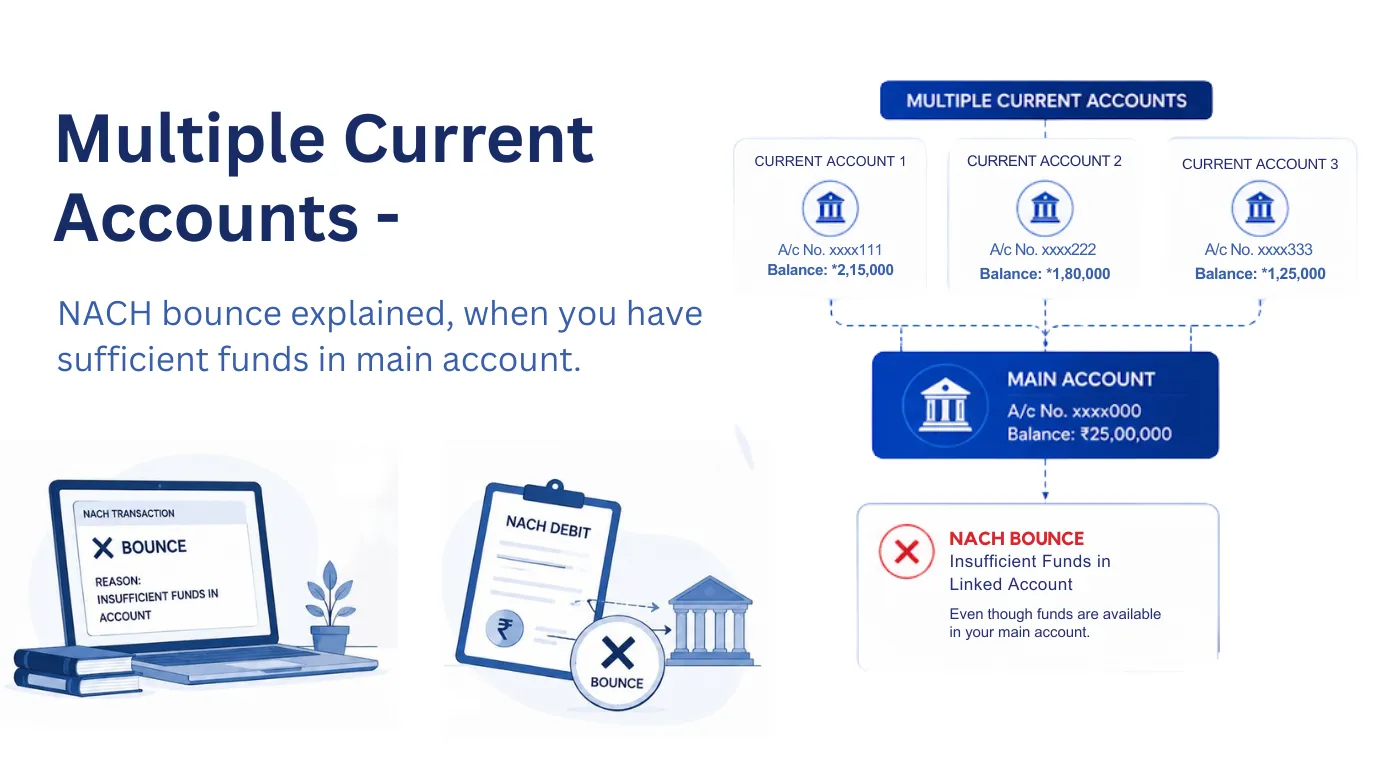

Split liquidity patterns are common when companies grow and manage cash inflows and vendor outflows across multiple banking architectures. It is very common to have a primary operational current account for bulk client inflows and secondary accounts for specific vendor payments or automated loan repayments. The big operational risk is when the automated NACH or auto debit mandate hits a secondary account which was temporarily unhedged and causes a localized bounce flag even when your primary account is sitting on huge liquidity reserves.

When this happens, the automated risk scoring models of external credit institutions detect a funds-based default flag that ruins your internal credit rating. The algorithm considers the single account transaction as a single event.

If you want to save your corporate file during the underwriting of a high-ticket loan, you need to build a Combined Macro-Liquidity Ledger. You want to show the credit committee that the bounce was a local clerical tracking error, not an institutional cash shortfall. You want to show that on that particular day your aggregate liquidity across all bank portals was well above the debit value.

A Real-World Example

A corporate firm prints out large monthly volumes of transaction. They keep their primary cash liquidity of ₹60 Lakhs in their main current account. However there was an old automated machinery loan EMI of ₹1.5 Lakhs mapped via NACH to an old secondary account. Due to an internal accounting delay , a transfer of client invoice to a secondary account was due before the automated debit date . Due to insufficient funds , the EMI mandate bounced .

The lending bank’s risk desk flagged the corporate profile for credit hunger and poor capital management right away.

The company compiled identical timestamped vector bank statement logs from both current accounts for that one 24-hour period to clear the file. They gave a unified day-end ledger of combined cash balances, proving that their net corporate liquidity was comfortably over ₹58 Lakhs at the exact hour the auto-debit failed. The empirical evidence confirmed the bounce was an administrative accounting error and the credit desk was able to override the negative automated entry and approve the facility.

Operational Key Learnings

- The Isolation Penalty: Risk engines treat each bank statement string of an account as a separate entity and any localized drop in balance is treated as a very strong indicator of a default.

- Unified Asset View: Aggregate your cross-bank statements into a single daily cash volume report to effectively demonstrate your macro-debt servicing ability.

- Immediate Remediation: Resolve any multi-account auto-debit failure with immediate bank transfers on the same banking day to maintain your corporate credit standing.

Enjoying our insights? Never miss an update on Google Discover or Google Reads. ➜