Lenders are under immense pressure: Banks, NBFCs, and private debt funds have annual lending targets (Priority Sector Lending, overall loan book growth, etc.). If they are lagging behind by February, they become highly aggressive in March to disburse funds to meet their year-end goals and secure performance bonuses.

1. The Tax Shield Advantage (Crucial for India)

This is the primary driver for year-end funding. In India, interest paid on business loans is a tax-deductible expense. Furthermore, assets put to use before March 31st gain depreciation benefits for the current year.

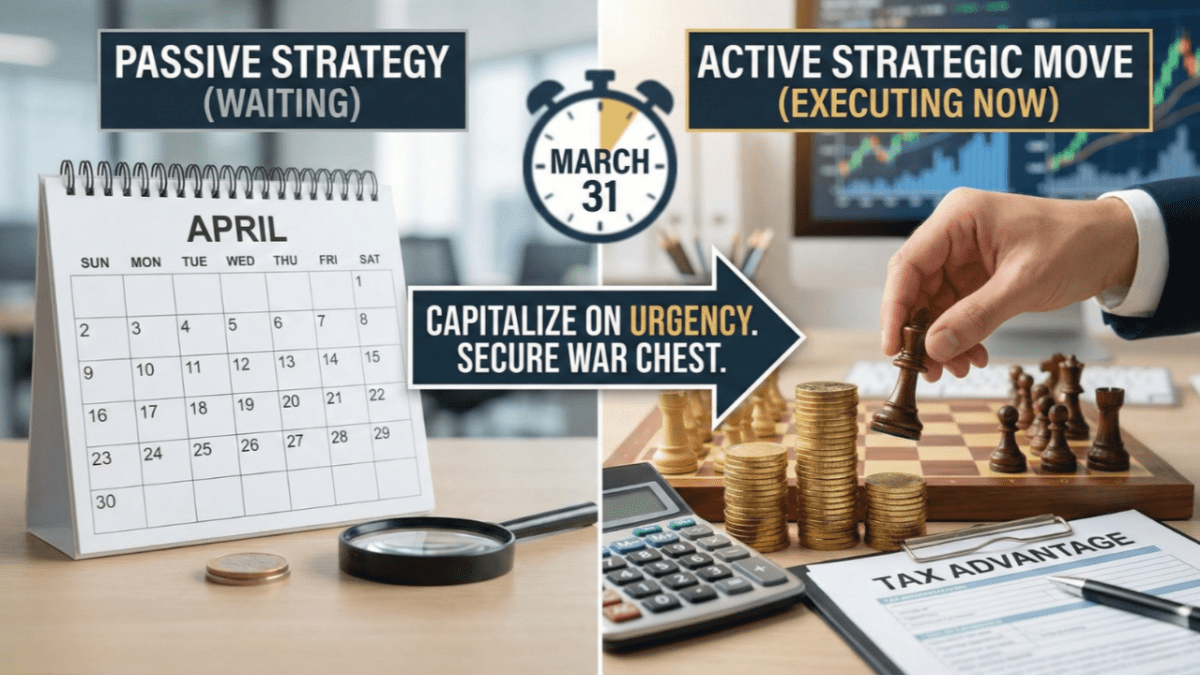

Why Now?

If you take a loan and deploy it before March 31st, you can book the interest expense and asset depreciation in this current financial year, instantly reducing your taxable profit. If you wait until April 1st, that tax benefit is pushed a full 365 days into the future.

2. Connecting Your Funding Purposes to the Year-End Strategy

Let’s look at how your specific funding needs benefit from this timing:

A. Asset Acquisition & Technology/Infrastructure Upgrades

- The March Advantage: If you buy machinery, vehicles, or IT hardware and ensure it is “put to use” before March 31st, you can claim depreciation for the current year. Even if used for less than 180 days, you get 50% of the standard depreciation rate.

- Why wait for New FY? Waiting until April means losing an entire year’s worth of tax shielding on that heavy CapEx.

B. Debt Refinancing

- The March Advantage: This is the perfect time to clean up the balance sheet before it is audited. By using cheaper long-term debt to wipe out high-cost short-term liabilities (like unsecured ODs or vendor credit) in March, your year-end financial ratios (Debt-to-Equity, Current Ratio) look significantly healthier to auditors and investors.

- Why wait for New FY? You will carry the expensive debt and poor ratios into the final audited balance sheet of the current year.

C. Inventory Management

- The March Advantage: Many suppliers offer aggressive “year-end discounts” in March to clear their own stock before closing their books. Securing funding now allows you to bulk-buy inventory at the lowest possible price points.

- Why wait for New FY? April often brings price hikes due to inflation, new government policies, or refreshed supplier price lists.

D. Market Expansion and Marketing

- The March Advantage: If you plan a major launch in Q1 of the new year (April-June), you need the war chest ready now. Booking marketing expenses (like advance payments for ad campaigns) in March can also help in managing current year profits for tax purposes.

- Why wait for New FY? If you start the loan application in April, you might not get funds until May or June, delaying your expansion plans and missing the Q1 momentum.

E. Initial Working Capital (For new verticals/subsidiaries)

- The March Advantage: If you are launching a new unit in the new FY, securing the “burn rate” capital in March ensures you hit the ground running on Day 1 of the new year without cash flow stress. Lenders are also keen to show new client acquisition in their year-end reports.

3. The Operational Reality: Speed and Negotiability

Beyond taxes, there are practical reasons why waiting for the new financial year is often a mistake.

- Faster Processing (Now): In March, credit committees meet frequently, and file movement is rapid because everyone wants to disburse before the deadline.

- Slower Processing (April onwards): April is typically a slow month in Indian banking. Staff are involved in year-end audits, transfers happen, and new targets haven’t sunk in yet. A loan process that takes 15 days in March might take 45 days in April/May.

- Better Terms (Now): To meet targets, lenders might waive processing fees, offer slightly better interest rates, or be more flexible with collateral requirements in March just to get the deal done. In April, that urgency is gone.

Stay Ahead of the Market

Get these updates directly on Email. No spam, just critical financial alerts.

Enjoying our insights? Never miss an update on Google Discover or Google Reads. ➜